A City-wide Analysis of 2026 Real Estate Assessment Increase Shows Who is Paying for the FY2027 Real Estate Tax Increase

Photo: The City Assessor’s office at Gage House, Cherry Hill Park.

By Peng Highnam and Robert Speir

Summary

The Falls Church Pulse pulls together data from the City’s FY2027 budget and the 2026 real estate assessments to analyze the impact of the 2026 assessment increases on taxpayers.

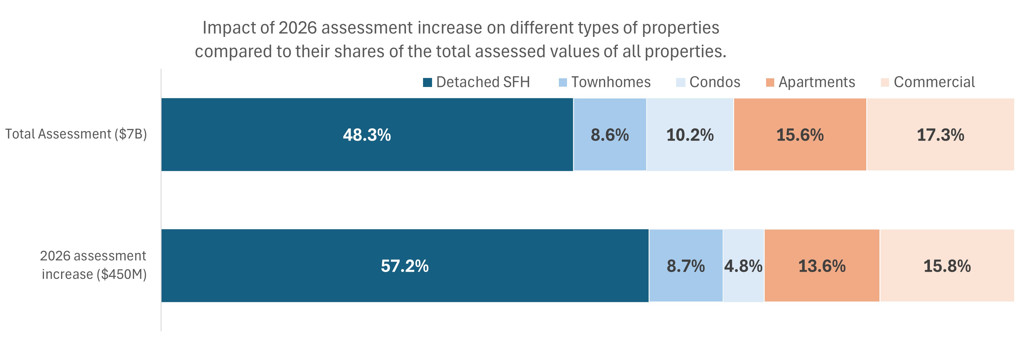

The $5.2 million increase in real estate tax revenues is disproportionately paid by detached single-family homeowners (SFH), especially in neighborhoods with the largest assessment increases. These properties form less than half of the City’s total taxable real estate portfolio but will pay 57% of the tax increase.

The assessments growth, excluding new construction, by real estate category is as follows:

- 8.1% Detached SFH

- 4.9% Townhomes

- 3.2% Condos

- 4.9% Apartments buildings

- 2.3% Commercial

Among SFH, the neighborhood median assessments growth varied from 0% to 15%. Taxpayers in high-growth neighborhoods will bear a higher burden of the tax increase.

The City Assessor bases assessment adjustments on neighborhood sales data, but more than half the neighborhoods had only one or no sales in 2025.

Background

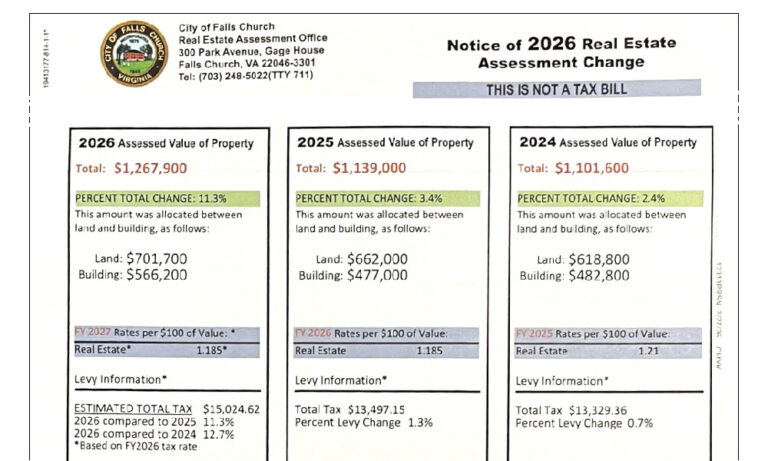

The 2026 real estate assessments were printed March 12, 2026, and homeowners received them the following week. Many were shocked by double-digit increases, contrary to the estimate of 6% anticipated in December’s FY2027 budget guidance presentation’s. To be fair, City Finance Director David So gave the overall assessment value increase from the Assessor’s Office without a breakdown of assessment increases by real estate type.

We decided to acquire the City’s assessment data files, available from the City Assessor for a $100 fee, and perform a data dive to get a clearer picture of 2026 assessment increases compared to 2025. We present our findings here.

Note that our findings do not exactly match some statistics cited in the budget due to the lack of documentation provided with the data files we received. There may be small differences in how properties are categorized and omitted. For example, we do not include properties that are partially in the City. We also filtered out properties that were in the data files but not in the City’s online database. These differences should not affect the assessments growth significantly.

We have interpreted the data in the files without any guidance from the Assessor’s Office. We checked that the numbers of properties for single-family homes, townhomes, and condominiums were consistent with the numbers reported in the Stephen Fuller Institute report, a study that catalogues housing in the City to forecast student enrollment in the Falls Church City Public Schools.

Higher assessment increase means higher tax increase

At the March 23, 2026, City Council meeting, City Manager Wyatt Shields presented his proposed FY2027 budget with a 6.9% increase in total assessments. That $450 million increase in total assessments translates into higher real estate tax revenues than were projected in December 2025. Assuming that the current tax rate of $1.185 per $100 of assessed value remains unchanged, the revenues increase amounts to $5.2 million. This increase was a welcome relief to Mr. Shields and the School Board; it was less welcome to those bearing the cost of the assessments increase.

Who pays for the tax increase depends on whose assessments have gone up. If one property’s assessment is unchanged for 2026 and another’s went up by 10%, the latter is paying for the City’s tax increase while the former is not. If two properties had equal assessments in 2025, but one’s assessment went up 10% while the other went up only 5%, the former will pay double the share of the overall tax increase compared to the latter. Thus, the tax increases disproportionately impact taxpayers.

The City Assessor published a summary of assessments increases for the FY2027 budget. The overall increase for each category of real estate is shown in the table below. We also include the increase that we at the Falls Church Pulse computed from the data files provided by the City.

| Assessment Increase | City Assessor | Falls Church Pulse | Explanation |

| Detached SFH | 8.1% | 8.2% | |

| Townhomes | 7% | 6.9% | |

| Condos | 3.2% | 3.1% | |

| Apartments | 6.3% | 5.9% | New construction discrepancy. Existing apartment buildings grew 4.9% in both City and Pulse data. |

| Commercial | 6.5% | 6.4% | Possibly missing new properties. |

There are small discrepancies between these data sources that reflect the margin of error in our analysis. We suspect much of the discrepancy is from newly constructed properties. For example, our computed assessment increase for existing apartment buildings matched the City Assessor’s stated 4.9% increase, but when new construction is included the Assessor’s increase is 6.3% compared to 5.9% in our data. Nevertheless, the discrepancies are not large enough to significantly alter the data in previous graphs.

The assessment increases range widely from 3.2% for condos to 8.1% for SFH. That implies that SFH will pay a larger share of the $5.2 million tax revenue increase than their portion of the City’s overall real estate portfolio of taxable properties. SFH make up less than half of the City’s total assessment value of $7 billion, but they will pay 57% of the tax increase. Condos will pay only 4.8% of the increase despite comprising more than 10% of total assessments. The graph below shows that the tax increase is not proportionately shared among property owners because of the different assessment growths across real estate types.

The varying growth of existing properties

| Market Growth | |

| Residential | 6.2% |

| – Detached SFH | 8.1% |

| – Townhomes* | 5.4% |

| – Condos | 3.2% |

| Apartment Buildings | 4.9% |

| Commercial | 2.3% |

The assessment increases above include new construction. The “market growth” table shows the growth for existing properties published by the City Assessor, except the Townhomes market growth is computed by us. There were no new condos constructed in 2025 and the few new detached SFH do not significantly change the overall growth rate. Within the residential category, there is a large difference among the market growth for SFH, townhomes, and condos. The market growth of SFH is 50% higher than the next highest category, townhomes.

For FY2027, the General Government operating budget increased 3.4% while the School Board transfer increased 4.1%. The assessment increases for commercial properties and condos, hence taxes, have not kept up with the cost of the City’s operating budgets. In this way, the other property owners are subsidizing condo and commercial property owners in paying for the increased cost of the Schools and the City government. This has been the trend in recent years.

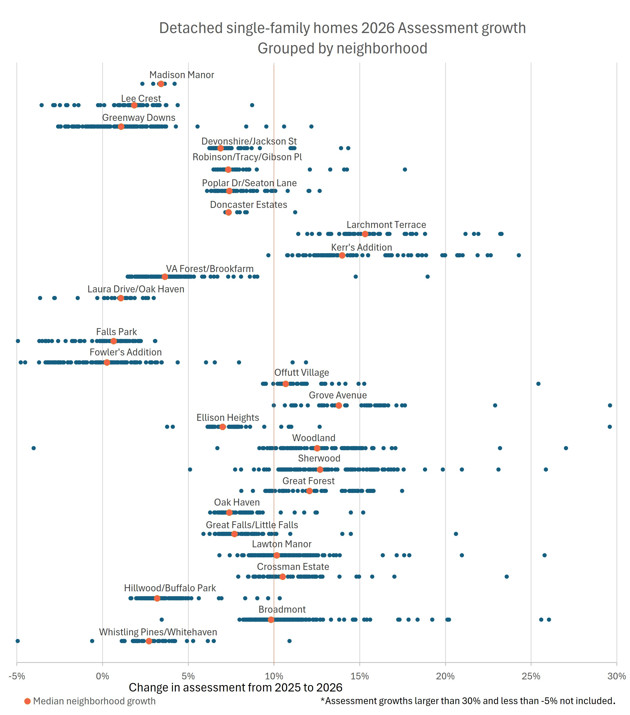

Distribution of individual assessments

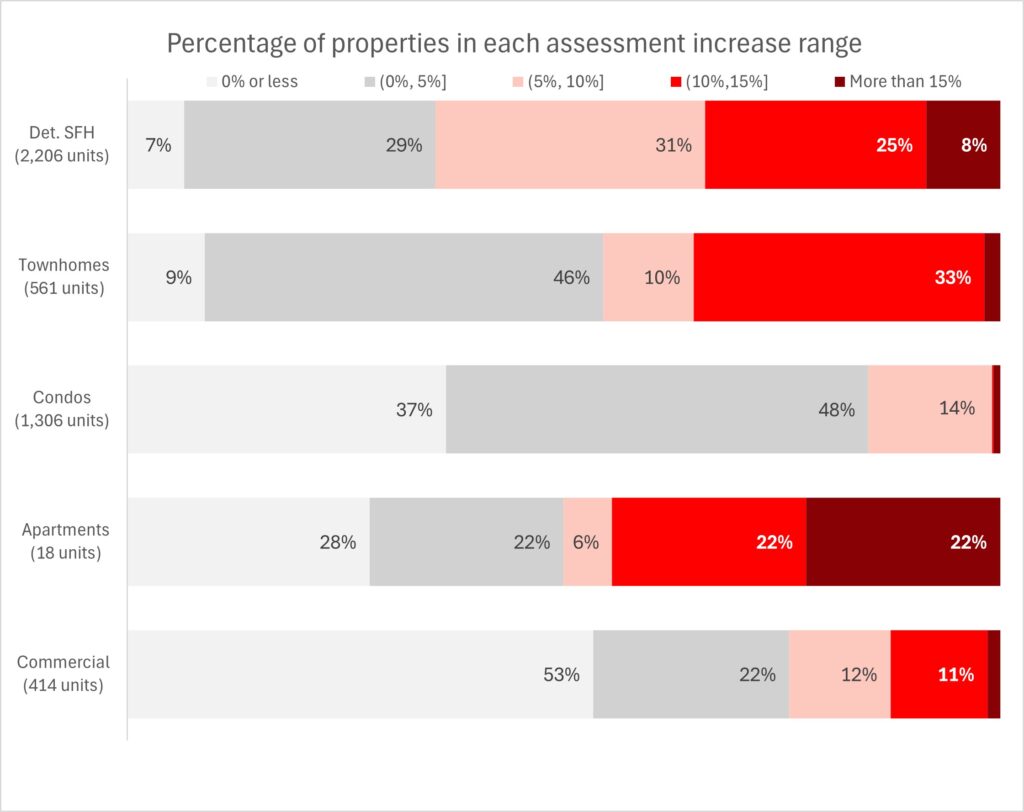

The assessment increases above represent the total assessed value increases of the properties in each category. Clearly, an individual property’s assessment increase varies within any particular category. The graph below summarizes the increases for individual properties for each category that are entirely within the City limits.

Twenty-nine percent of 2,206 detached SFH had assessment increases of more than 0% and up to 5%. Thirty-three percent, or a third, increased more than 10%. Thirty-one percent had increases of more than 5% up to 10%. There was either no change or a decrease in assessments for 7% of the SFH.

Townhomes showed a marked division in assessment increases. More than half had 5% or lower increases, while 35%, made up primarily of 194 Winter Hill townhomes plus three others, had increases of 10% or more.

Eighty-five percent of condos and 50% of apartment buildings had increases of 5% or less. We did not include eleven Virginia Village apartment buildings in this analysis as they are considered affordable housing. Their assessments were unchanged.

Fifty-three percent of commercial properties had no change or decreases in their assessments. Commercial properties with more than 10% increases included both new and old properties.

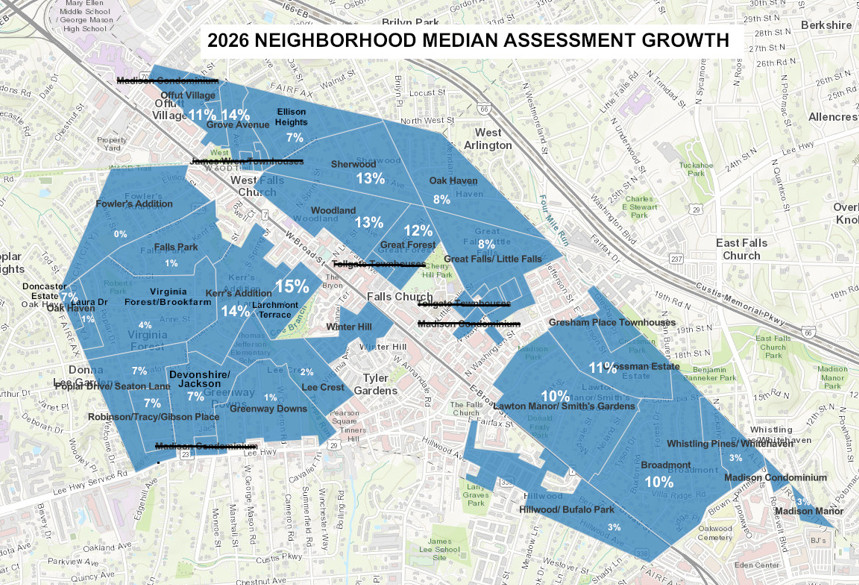

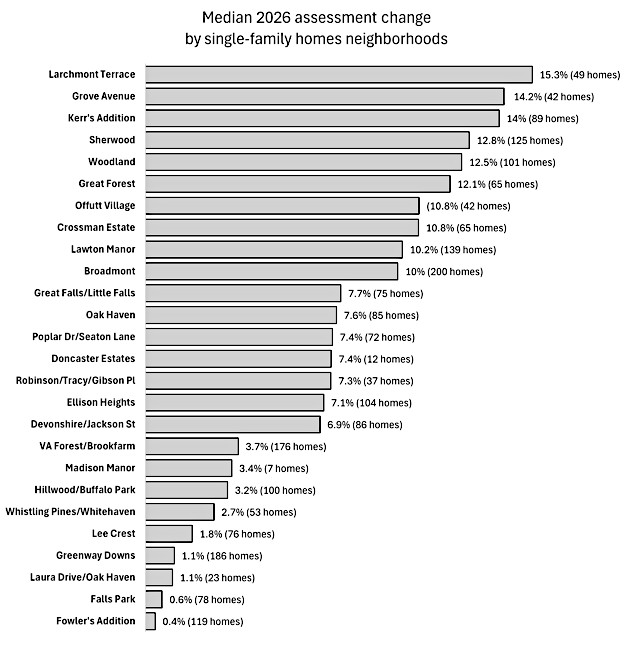

SFH assessment increases varied by neighborhood

Overall, SFH assessments increased by just over 8%, but there is wide disparity between neighborhoods with assessments in some neighborhoods barely changing while others increased by more than 14%. The bar graph shows the median assessment increase by neighborhood, and the map shows the locations of the neighborhoods.

Assessments are made up of two components – the land values and the improvement values (buildings, man-made structures). All but two properties in our SFH dataset received a 6% increase in land value. (This is consistent with past history that land values are treated the same across all neighborhoods, as reported in our land values post.) But the increase in improvements (mostly the homes’ values) varied greatly from neighborhood to neighborhood. In neighborhoods where the median growth barely grew, many improvement values were lowered from 2025. On the other hand, the median change in improvement value of the Larchmont Terrace neighborhood was 31%.

We plotted the assessments of each SFH organized by neighborhood in the scatter graph below. A blue dot may represent more than one SFH of the same value in the same neighborhood. In each neighborhood, the red dot represents the median growth for that neighborhood. The graph does not show properties with increases larger than 30% or decreases of more than 5%.

We investigated outliers in the Woodland neighborhood to understand the spread within a single neighborhood. The one property with a 6.7% increase, much lower than the median of 13%, was sold in 2025 at 21% above its assessed value. One property had its assessment reduced because it is undergoing extensive renovations and, therefore, is uninhabitable. One of the two properties that increased more than 20% completed an addition, but we could not find an obvious reason for the high increase of the second property, a home built in 2022.

Assessment growths based on low number of neighborhood sales

From the City’s Real Estate Assessment Frequently Asked Questions:

“How do trends in real estate prices affect assessments?

Normally, a property’s assessment is based on sales activity in a defined neighborhood. The assessed value of a particular property depends on the sales of other properties in the nearby area. Due to limited sales, neighborhoods may be grouped together to determine the change in assessment values for all of the properties in those collective neighborhoods. The January 1, 2025, assessment relied on sales between January 1, 2024, thru December 31, 2024.”

The table below is a compilation of the 2025 SFH sales that are listed in the City’s property database and designated “Valid Sale” for purposes of determining assessment values the following year. ASR refers to the ratio of the assessed value of a property to its sales price, and the average ASR is for the sales in each neighborhood, if any. The median growth is the median assessment change of all homes in that neighborhood.

From this table, it becomes clear that there are very few sales in most neighborhoods to form a basis for changing the assessment values of all homes in a neighborhood. Over half the neighborhoods have zero or only 1 sale. These total 994 properties or 45% of the City’s SFH. Even when grouped together, the wider Broadmont area that includes Lawton Manor and Crossman estates had only four sales. Kerr’s Addition and Larchmont Terrace, with two sales only, seem to have been singled out for 14-15% increases compared to their surrounding neighbors (0-7%) in the area around Oak Street Elementary School.

| Neighborhood | No. of Homes | No. of Sales | ASR Average | Median Growth |

|---|---|---|---|---|

| Larchmont Terrace | 49 | 1 | 0.73 | 15.3% |

| Grove Avenue | 42 | 1 | 0.72 | 14.2% |

| Kerr’s Addition | 89 | 1 | 0.77 | 14.0% |

| Sherwood | 125 | 4 | 0.83 | 12.8% |

| Woodland | 101 | 6 | 0.83 | 12.5% |

| Great Forest | 65 | 0 | – | 12.1% |

| Offutt Village | 42 | 3 | 0.89 | 10.8% |

| Crossman Estate | 65 | 2 | 0.83 | 10.8% |

| Lawton/Smiths | 139 | 1 | 0.76 | 10.2% |

| Broadmont | 200 | 1 | 0.48 | 10.0% |

| Great Falls/Little Falls | 75 | 1 | 0.98 | 7.7% |

| Oak Haven | 85 | 5 | 0.82 | 7.6% |

| Poplar Dr/Seaton Lane | 72 | 6 | 0.76 | 7.4% |

| Doncaster Estates | 12 | 0 | – | 7.4% |

| Robinson/Tracy/ Gibson Pl | 37 | 4 | 0.89 | 7.3% |

| Ellison Heights | 104 | 3 | 0.83 | 7.1% |

| Devonshire/Jackson St | 86 | 0 | – | 6.9% |

| VA Forest/Brookfarm | 176 | 7 | 0.84 | 3.7% |

| Madison Manor | 7 | 0 | 0 | 3.4% |

| Hillwood/Buffalo Park | 100 | 4 | 0.96 | 3.2% |

| Whistling Pines/ Whitehaven | 53 | 1 | 1.01 | 2.7% |

| Lee Crest | 76 | 1 | 0.83 | 1.8% |

| Greenway Downs | 186 | 7 | 0.93 | 1.1% |

| Laura Drive/Oak Haven | 23 | 1 | 0.99 | 1.1% |

| Falls Park | 78 | 1 | 0.92 | 0.6% |

| Fowler’s Addition | 119 | 6 | 0.92 | 0.4% |

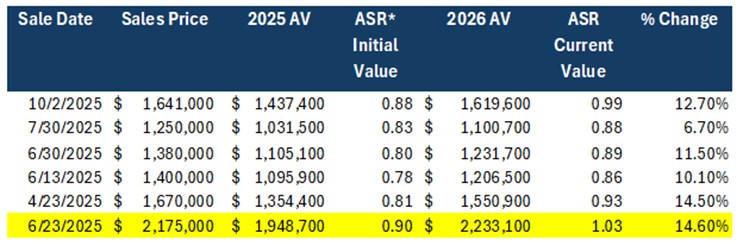

Obfuscating a case of over-assessment?

In response to the following question in the FY2027 Budget FAQ document:

“10. Given some very high percentage increases in residential assessed values that are already the subject of neighborhood chats, I’d like to understand how many residential properties saw their assessed values increase by 10% or more. …

A: Excluding new construction, 20% of residential properties are growing at over 10%. The primary driver of the increase for this year was due to the fact that higher sales values in the City has driven the higher increase in assessed values along with 2025 AV’s did not grow as significantly as it should have. We’ve pulled data from one neighborhood as an example:

Based on this data, houses sold in 2025 were assessed at a much lower value based on the sales data. In 2026, the assessments not only increased the AV’s to be closer valued to their sales data, but the surrounding houses also increased in their AV’s. …”

In making its case, staff published the table in the budget document and omitted the 6/23/2025 sale, highlighted in yellow, for that neighborhood. (The neighborhood is Woodland.) When that sale is included, it tells a different story – the neighborhood increase for Woodland resulted in that property being over-assessed. It shows that the assessment model is a coarse tool that results in some number of over-assessments. Of the 67 “valid sales” in 2025, 14 (21%) of those have 2026 assessments that exceed their sales prices.

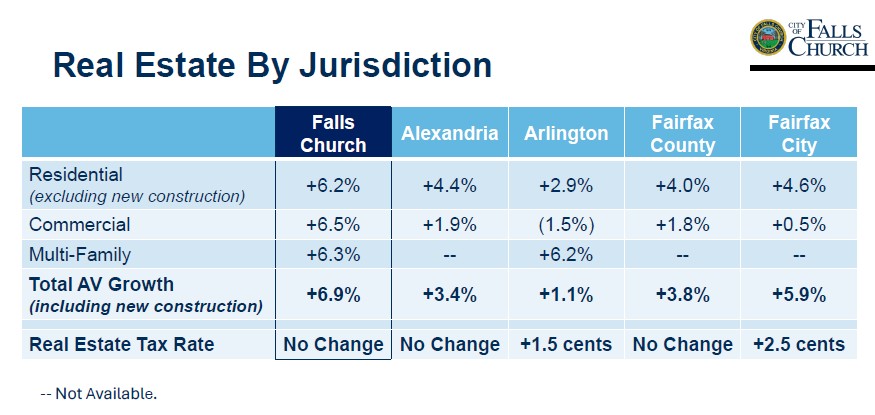

How do we compare with neighboring jurisdictions?

At the March 23, 2026, City Council meeting, Mr. Shields presented the table below that compares assessment increases in Falls Church City with our neighbors. The City’s residential assessment increase is almost double that of Arlington.

Fairfax County’s SFH increased 4.28%, almost half of the 8.3% SFH here, but condo increases were similar. In the Dranesville district of Fairfax County that includes McLean and Tysons, the average increase was 4.9%. (Source: Fairfax County FY2027 Budget Presentation.)

We could not find more detailed information on Arlington County and invite you to explore the Arlington County assessment databases online to investigate their assessment increases. Our cursory look at properties in the immediate vicinity of the City showed increases of 2-3%.

Thinking of contesting your assessment? Final date is June 5.

Even though assessments were sent out over a month later than usual, the City has not changed the assessment appeal due date. Property owners who did not file an appeal with the Assessor’s Office can file an appeal to the Board of Equalization by June 5. The Pulse post on filing an appeal provides some tips, Thinking of Filing an Appeal of Your 2026 Assessment? Here Are Some Tips, April 8, 2026.