City Staff, Council Explore Applying a Commercial and Industrial (C&I) Real Estate Tax

Summary

Counties and cities that are members of the Northern Virginia Transportation Authority (NVTA) may impose an additional real estate tax of up to 12.5 cents per $100 of assessed value on commercial and industrial properties to be used for transportation projects. NVTA members that impose a Commercial & Industrial (C&I) tax or set aside an equivalent amount from other funds (C&IE) can increase their share of NVTA 30% funds for local transportation projects.

Currently, the City has opted for the C&IE, setting aside $1.4 million from general revenues in FY2026. About 70% of general revenues are real estate taxes; only about 13% are currently from commercial properties. The question, then, is whether other taxpayers in the City should be contributing to a tax that was intended for commercial property owners.

Commercial real estate taxes have been flat or increased slowly over the last decade, unlike the steep surge experienced by residential properties, a result of differences in long-term market trends. The weight of the City’s taxes has shifted away from commercial properties and toward single-family homes and condominiums. A C&I tax could rebalance this tax burden to some extent.

Complicating this issue is that adopting the C&IE option allows the funds to be applied to the City’s required subsidy for WMATA ($1.2 million) whereas a C&I tax may not be so applied. C&I taxes must be used to expand road infrastructure and transportation and may not be used for maintenance or transportation subsidies.

Background

The City’s move to impose trash fees on households that use that service instead of paying for the cost of solid waste services from general revenues surfaced the issue of tax equity. Questions were raised about the C&I tax on commercial real estate, intended to reduce the tax burden on residents, but currently paid from City revenues collected mostly by taxing homeowners.

At the request of City Council members, staff presented a review of the C&I tax at the November 14, 2025, City Council Budget and Finance Committee meeting.

The Commercial and Industrial (C&I) Real Estate Tax

The State of Virginia (Section 58.1-3221.3 ) allows the member localities of the Northern Virginia Transportation Authority (NVTA) to impose a C&I tax up to 12.5 cents per $100 of assessed value of commercial and industrial property, excluding commercial property that is used for residential purposes, such as apartments and senior living establishments. These taxes are to be used for transportation projects only. In the case of mixed-use buildings, the commercial areas of these structures would be taxable, but the apartments would be exempt. Localities may opt to set aside the equivalent amount (C&IE) from other revenues instead of taxing commercial properties.

Localities that either impose the C&I tax or opt for C&IE are able to access a greater share of NVTA funds for local projects, called NVTA 30%. NVTA receives funds from the State, including a 0.7% sales tax as well as State income taxes and transportation fees. 70% of NVTA funds are for regional transportation projects, and the remaining NVTA 30% is shared among members for local transportation projects.

City opted for C&IE

According to City staff, all NVTA member localities have opted for either the C&I or the C&IE except Loudon County and Alexandria. Arlington County, Fairfax County, and the City of Fairfax have chosen to impose the maximum 12.5 cents C&I tax rate on commercial properties. Falls Church has opted for the C&IE.

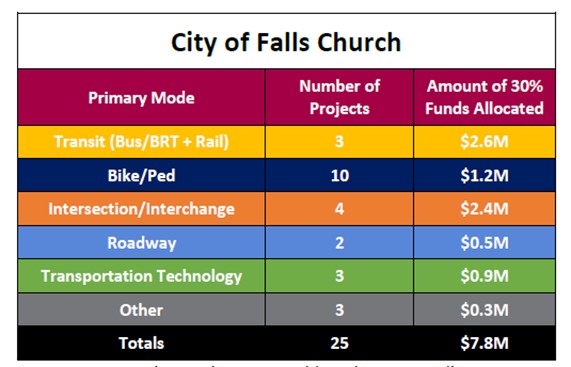

In FY2026, $1.4 million was designated for C&IE and used to cover the WMATA subsidy of $1,245,000 and $167,000 for new sidewalks as part of the City’s Missing Links program. The $1.4 million represented the equivalent of 12.5 cents in the real estate tax rate on commercial and industrial properties in the City so that a greater share of the NVTA 30% funds is available. The City has been using the NVTA funds as a match for State funds in many transportation projects. The NVTA website has the latest list of projects funded in the City, available here.

Restrictions on how C&I taxes are used

C&I taxes can only be used for transportation projects that add or expand capacity, service, or access. These include adding bike lanes, signals, sidewalks, new bus stops, and new roads.

Roadbed reconstruction, a sizable expense for the City’s aging roads, is unfortunately considered maintenance and so is not eligible for NVTA funds.

City Manager Wyatt Shields also explained that an advantage of the C&IE option is that it has fewer restrictions than C&I taxes on how the funds can be used. The City uses most of the C&IE to pay its share of the WMATA subsidy, a use that would not be permitted if the City switched to C&I taxes.

Budget and Finance Committee discussion

Council Member Marybeth Connelly reminded the committee that the issue came up during the solid waste discussions when the City reduced the real estate tax rate by 1.5 cents last year in exchange for solid waste fees on some residents, providing a windfall to commercial property owners. The question then was whether commercial property owners should pay the C&I tax separately to ensure that taxes are “equitable.”

Deputy Finance Director Melissa Ryman explained that the $1.4 million C&IE was equivalent to 2.25 cents of the real estate tax rate. Unlike solid waste fees, Mr. Shields said that switching to a C&I tax would not reduce the tax rate by 2.25 cents because the $1.2 million WMATA subsidy would continue to be paid from general revenues as it is not allowed to be paid under the C&I code. Any C&I tax should be considered new revenue for the City. The City can implement a mix of C&I tax and C&IE up to the 12.5 cent equivalent amount.

Mr. Shields suggested the crux of the matter is how the City would use C&I taxes with its restrictions, and that it is a policy issue for City Council. Council Member Laura Downs said it could be used to fund sidewalks.

Council Member Erin Flynn looked at the tax as an option for raising revenues for the City and distributing the costs in a different way. Mayor Letty Hardi said the C&I tax is just one tax lever, and she would prefer looking holistically at all the levers for raising revenues.

Economic Development Authority Chair Ross Litkenhous came out forcefully against imposing a C&I tax on commercial properties. He worried that that tax would have a detrimental effect on City businesses and that landlords would pass the tax increase on to tenants. “Disproportionately, residential contributes more to our public service cost than commercial. … Every business pays into just about every single bucket of tax revenue that we collect. … [we are] shifting most of this cost for all that to businesses that already pay more than their fair share,” he said.

Mr. Shields refuted Mr. Litkenhous’ claims, saying that the long-term trends in the City have been that the residential homeowners have contributed more to the City’s revenues because there has been a 20-year-plus trend of market values steeply increasing for residential properties. “The long-term trend in the City has been that our smaller property owners, which is to say our residential property owners, homeowners throughout the City, are paying proportionately more for the cost of services in the City relative to our large property owners,” he said.

“Proportionately, there is a rebalancing that is worthy of consideration as a public policy question. It came up in the context of the solid waste fee, where it was kind of raw, that costs were transferred from commercial owners to residential – no question that occurred, and it has been a longer-term trend over a decade,” Mr. Shields added. (His observations are corroborated by the Pulse’s analysis, Single-Family Homeowners Bear the Cost of the City’s Growth, December 3, 2025.)

Mr. Shields said that the commercial property base has maintained the same proportion in the City’s real estate property base only because of new construction. Valuations have not changed much over the years. For commercial properties that have not undergone major renovations, owners are paying the same or less taxes than they were 20 years ago.

Council Member Arthur Agin wondered if landlords would pass through any tax increase. Mr. Agin said he was also bothered that this does not affect the apartment buildings as commercial properties for residential use. Apartment real estate taxes have also grown very slowly.

The meeting concluded with members voicing a need for more discussion and analysis.

Investigating commercial assessments and tax payments

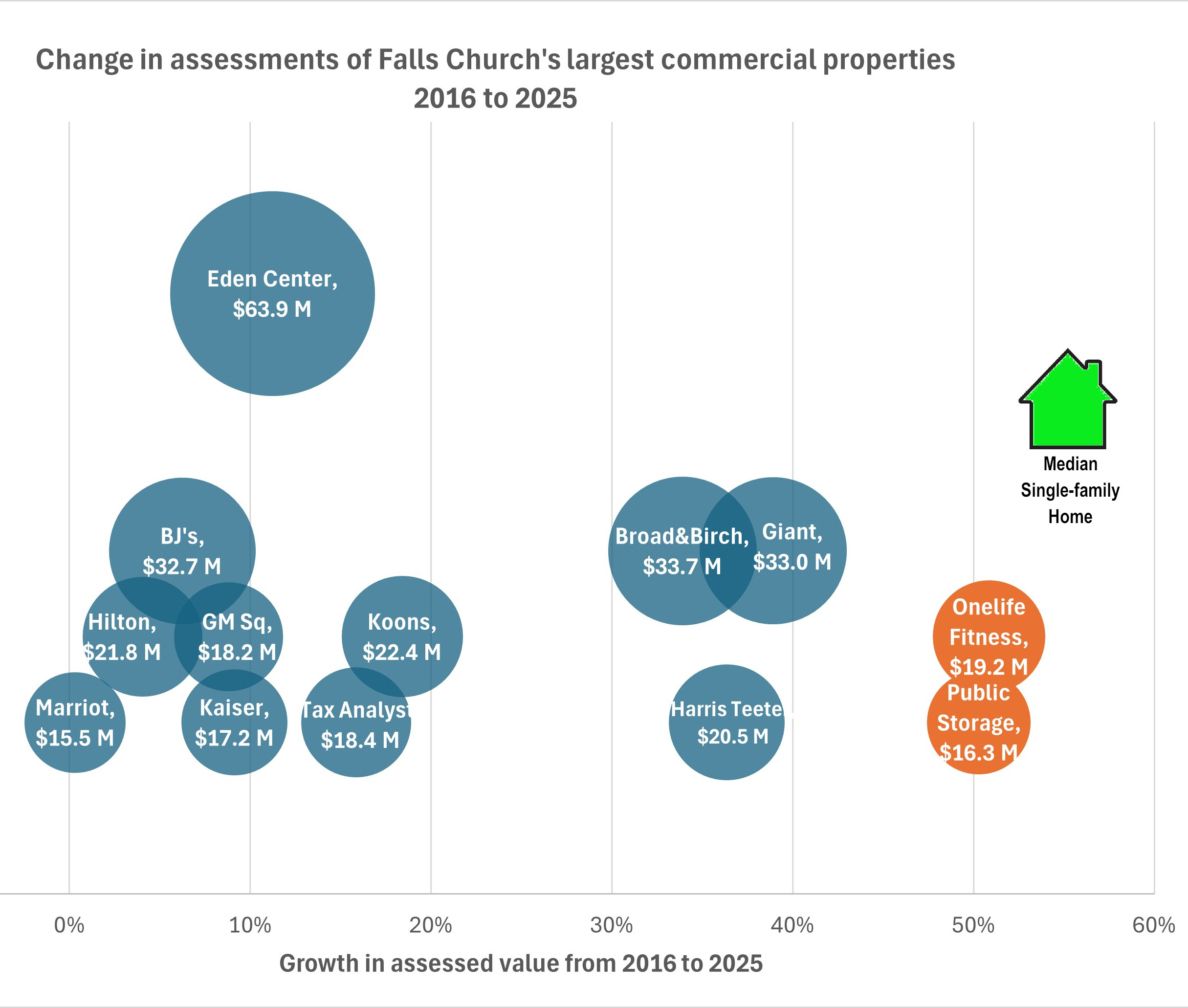

The Pulse researched the assessment history of the City’s commercial properties that were valued at over $15 million in 2025. Founders Row and West Falls were omitted because of their short histories. Also, the Kensington senior living facility was omitted because it would not be subject to C&I taxes.

The chart below shows how their assessment values have grown from 2016 to 2025. The size of the bubble reflects the assessed value in 2025. The largest property, Eden Center, is almost double the value of the next largest property and only grew 11%. Onelife Fitness and Public Storage both underwent major reconstruction that account for the 50% growth in their assessment values. Broad & Birch and the Giant shopping centers underwent a major facelift while Harris Teeter was newly completed in 2016. The remaining properties were unchanged or had minor alterations. Their valuations increased between 0% and 18%.

By comparison, the median single-family home value increased 55% during the same period. This difference in assessment growth has reduced the share of taxes paid by commercial properties and increased the share paid by residential properties.

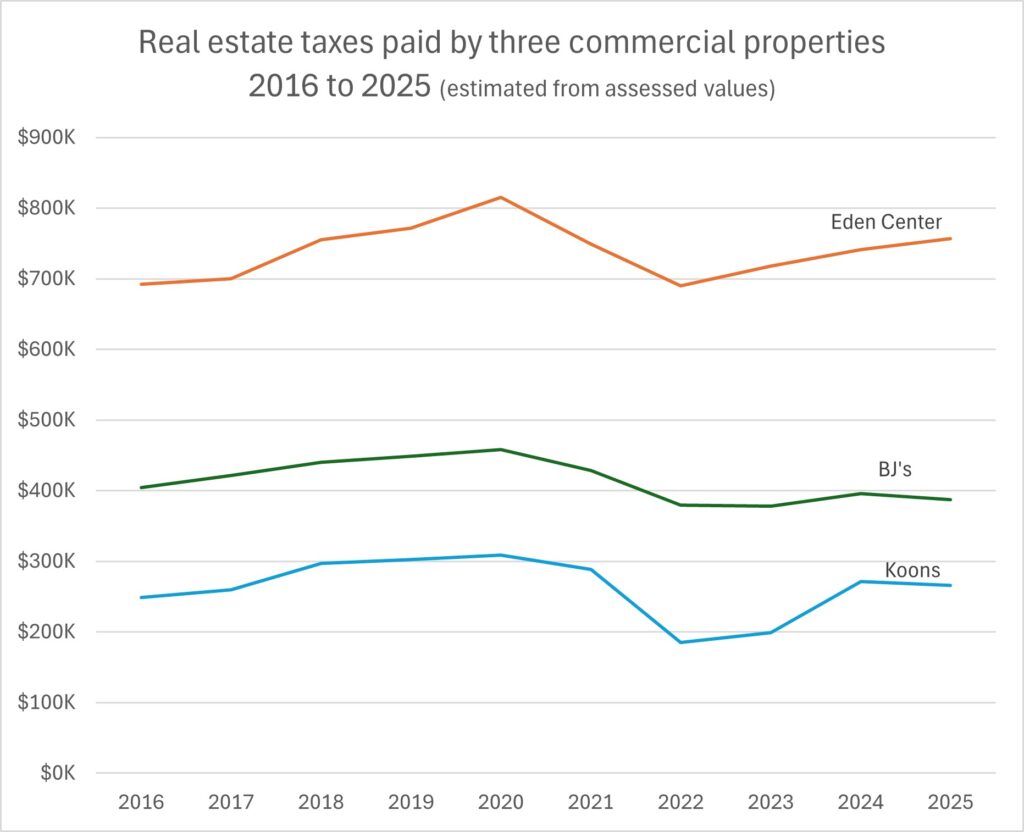

We estimated the taxes paid by three unchanged properties based on their assessed values for 2016 to 2025. The results are shown in the graph and support Mr. Shields’ observations.

The taxes paid by Eden Center and Koons barely increased while BJ’s taxes decreased. All three properties received large tax reductions after COVID and are still paying lower taxes than before COVID. Meanwhile, homeowners in the City have had tax increases every year. The median single-family home taxes increased almost 40% during this period.

It may be that any increase in real estate taxes on commercial properties would be passed on by landlords to tenant businesses. But over the last decade, leases at Eden Center have increased dramatically without any meaningful change in taxes, and notably led to the closure of the Center’s namesake Eden Supermarket. Low real estate taxes had no effect on leases. Market forces are more relevant.

References

- City Council Budget and Finance Committee meeting, November 14, 2025. (Starting at 27:28) This official video will not display properly on a small screen as it contains the agenda.

- Commercial and Industrial Real Estate Tax Update, November 14, 2025. Staff presentation.