Thinking of Filing an Appeal of Your 2026 Assessment? Here Are Some Tips.

By Robert Speir and Peng Highnam

Summary

With a third of detached single-family homeowners in the City of Falls Church receiving assessment increases of 10% or more, many may be considering an assessment appeal. To understand and research data for an appeal, homeowners need to request property cards and cost model sheets of their properties and neighboring properties. This is public information but can only be obtained by emailing the City Assessor.

At this writing, it seems that the Assessor’s Office has adopted a delaying or denial policy regarding information on the Cost Model Sheet that is necessary to understand assessment calculations. By referring property owners to file under the Freedom of Information Act process, they are likely in violation of §58.1-3331, (parts A-E) of the Virginia statutes.

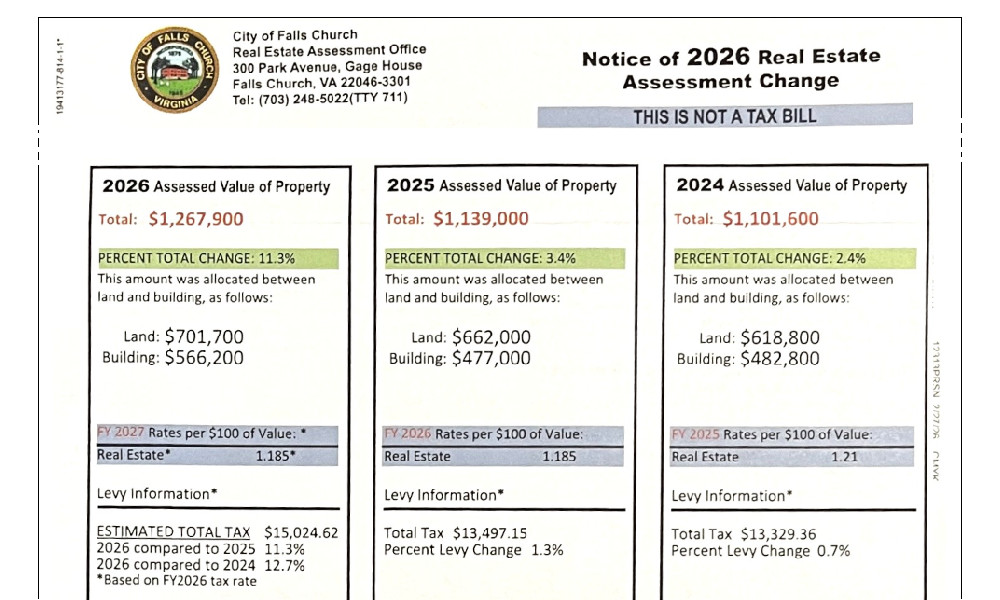

Assessment appeals to the City’s assessor must be filed by April 15, 2026, and appeals to the Board of Equalization must be filed by June 5. These dates have not been moved even though the 2026 assessments were mailed out over a month later than usual in mid-March.

The assessment appeal schedule

Falls Church’s Assessor’s Office conducted a “mass assessment” of residential properties in late 2025 and early 2026 that resulted in 2026 assessments. The assessments were not mailed to property owners until mid-March 2026. Despite the late mailing, the City has not changed the April 15 date for appealing assessments to the Assessor, although property owners have until June 5 to submit an appeal to the Board of Equalization (BOE).

2026 assessment increases shock many single-family homeowners

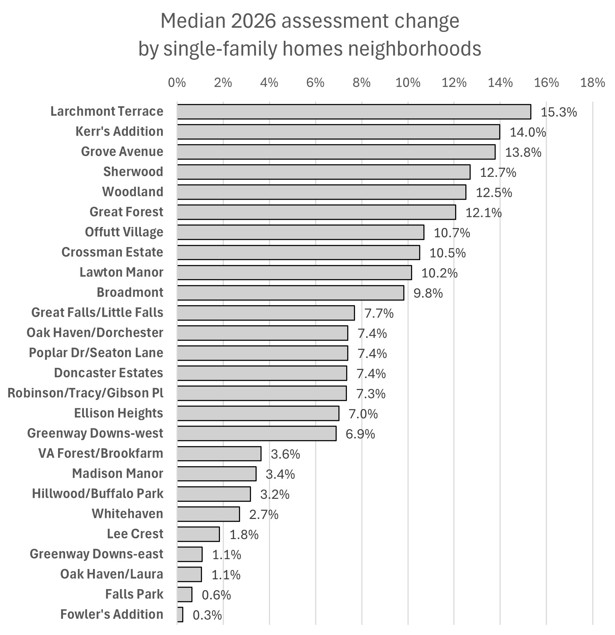

Upon receipt of their 2026 real estate assessments in March, many residents were surprised to see the extent of their increases from 2025. The average residential property assessment increased 6.2% but the graph below shows that the median increases for some neighborhoods of detached single-family homes (SFH) were as high as 15% while others were under 5%. Medians understate the extremes within neighborhoods; some residential assessments changed 5 to 8 percentage points higher or lower than the medians. Further, Falls Church City assessments increased significantly more than those of neighboring jurisdictions, especially for SFH.

The objective of the assessment process is to obtain reliable estimates of fair market value (FMV) for individual properties—including land, house, and ancillary structures such as decks, patios, and outbuildings. The methodology by which the City of Falls Church accomplishes this is logically and procedurally detailed, undocumented, and sometimes internally contradictory. Nevertheless, with data and information that, by law, should be available to all property owners, the methodology can be transparent and even allow comparisons between properties.

While we will examine assessment methodology, assumptions, and the 2026 data in forthcoming posts, our purpose here is to highlight sources of information that will help homeowners understand their own assessments. We have already explored the factors that affect land valuation; in the near future, we will focus on the non-land components of a property, or its “improvements,” as they are termed.

Information required to understand an assessment

With one-third of detached single-family homes receiving assessment increases of 10% or higher, many homeowners may be considering appealing their 2026 assessments. For anyone contemplating an appeal or who just wants to understand their assessment, three main sources of information are relevant:

- The Falls Church website’s online Real Property Database, actDataScout, provides a property’s description, sales, and assessment histories.

- The “Property Card” document attaches assessment monetary value to the various components of the online property description and shows how the assessment is calculated. Property Cards are public but must be requested from the Assessor’s Office by sending an email to realestateassessor@fallschurchva.gov.

- The “Cost Model Sheet,” is a one-page report that shows exactly how various external scaling factors are brought together to create the values on the Property Cards, i.e., the assessment itself. This may not be available for all properties for reasons we address below. Again, email the Assessor’s Office for this information.

You may need multiple Property Cards.

There should be no charge for these documents, nor should there be a need to file Freedom of Information Act (FOIA) requests. You may request as many of these cards as needed for your investigation. They can be identified by their Real Property Code (RPC) numbers from the property database or by their addresses.

- Obtain Property Cards for 2025 and 2026—This is the only way to see year-to-year changes that affected a property’s 2026 assessment, both the current year and previous year.

- Obtain Property Cards of other properties—This would be for comparisons, as in an appeal. If you are contemplating an assessment appeal, you should request these documents for all the properties that might be cited as comparables in the appeal documents.

The Cost Model Sheet has key information.

The Cost Model Sheet gives specific values for parameters such as a home’s build quality and neighborhood market factors that determine the dollar values given to improvement components of a specific property. The Cost Model Sheet is the only source of a key factor that induces the cost per square foot of a home to rise as its size decreases. Termed a “size adjustment factor,” this information is required for comparing assessments of houses and for understanding how much a size change will affect the assessment.

In the past, the Assessor’s Office has been less than willing to release the Cost Model Sheets. The reason usually cited is that since the document is not actually in the Assessor’s physical possession because it requires a computer interaction, its release is not required by Virginia statutes. This reasoning is specious at best. Everything a taxpayer obtains from the City requires computer interaction, including the assessments themselves. If this request fails, the specific components of the Cost Model Sheet clearly fall under Virginia statutes’ requirements for Assessors to provide, and can be requested, item by item, in a follow-on request. We will address this issue in a later post.

Understanding the sequence of appeals and hearings

Homeowners should make a serious effort file an appeal to the Assessor’s Office by April 15, even if it is incomplete. Property errors, both for a property, and for other properties that might relate to it indirectly, are not hard to find if present. Basements that are incorrectly described on the Property Cards can cost the owner hundreds of dollars a year in excess taxes. Or a single 2025 sale within a neighborhood that is excessively high compared to last year’s assessment might incorrectly raise assessments for the entire neighborhood. If time does not permit a thorough analysis, file anyway.

If the appeal is denied, then the property owner can refile with the Board of Equalization (BOE) by June 5, using better information. As noted in the Assessors Office pages of the City website, a property owner can send an appeal straight to the BOE (see “Appeals Process/Appeal to the Board of Equalization”). They should use the BOE forms from the Assessor’s website and as much data and analysis as possible. In all likelihood, the BOE will receive the Assessor’s review later in the summer. The point here, however, is that, if a BOE appeal is not filed by June 5, then the appellant loses the opportunity to pursue an appeal to override the Assessor’s denial.

When the BOE review season begins in the fall, the BOE will hold an organization meeting in which they will elect new officers and take up modifications to their “Rules of Procedure.” This quasi-legal document, redrafted or modified each year, is the BOE’s self-written contract on how it does business. One part of the document specifies lead times for delivery of hearing materials.

The Assessor, whose office provides BOE administrative support, is required to deliver to appellants and BOE members hearing packages that include all forms, the appellant’s June appeal justification, and the Assessor’s more recent rebuttal to it. Typically, the requirement was to require delivery to all parties 10 or more days before a hearing. That is the first time the appellant will have seen the case the Assessor will use to get the BOE to deny an appeal.

The ability to offer additional material after an appeal is filed

Taxpayers should be aware of some misleading information regarding BOE appeals. In one critical area, for the last three years, the BOE has corrected City attempts to dictate that BOE appellants cannot offer any additional (written) material after the BOE appeal is delivered in June.

Since 2023, BOEs have recognized that this limitation effectively precludes appellants’ abilities to rebut freely the Assessor’s arguments against their appeals. Under the old Rules, the Assessor had the only materials the appellant could submit, and had five to seven months to develop and refine a rebuttal before the hearing. The appellant had only a few days to study the rebuttal and was not given the chance to present a counter argument to the Assessor’s case.

Accordingly, in 2023, the BOE changed its “Rules of Procedure” guarantee that the appellant can develop and distribute new material in response to the Assessor’s case after receiving it about 10 days before a hearing. Then, the appellant can present a rebuttal in the hearing. While it is not possible at this point to say what the next BOE might decide, this precedent suggests that an appellant will have the capability to further develop their appeal during the 10 days before the hearing, thereby making the hearing less one-sided.

Understanding your rights as a homeowner

It is important for every interested taxpayer to understand their rights under Virginia statutes. These rights relate directly to the matter of interpreting assessments. To that end, we recommend reading Code of Virginia, § 58.1-3331 “Public disclosure of certain assessment records.”